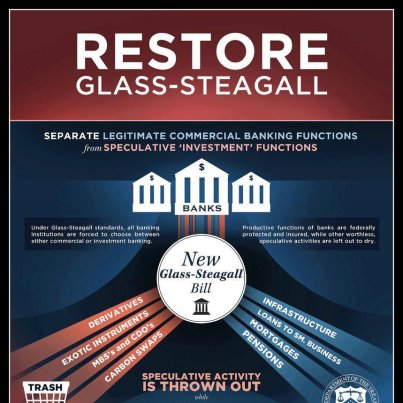

THE NEW GLASS STEAGALL

This drawing is making the rounds on the intertubes and I find myself going "mmmm" when I look at it. It stems from a understandable frustration with the banking system but gets the problem and the solution wrong imho.

Glass Steagall doesn't say anything about derivatives.

Glass Steagall didn't really say anything about derivatives for the very simple reason that they didn't exist back then. Nor are they really the problem

From what I remember, GS was mainly about 2 things

A/ Separation of commercial and investment banking.

The a/ part is pretty straight forward and says commercial banks shouldn't gamble with deposits. Once that gambling is removed then insurance of deposits makes sense. Clinton removed Glass-Steagall under lobbying pressure because large banks wanted to have speculative operations, like traditional investment banks, but also wanted to keep their commercial operations. Note that (for the most part) they were not gambling with deposits and were playing with their own capital. IT ISN'T WHAT CREATED THE CRISIS....

B/ Regulation of monetary levels

The second part is not addressed in the drawing and the authors see vaguely through the fog, let me see if I can help. The GS regulation fixed the ratio of outstanding debt to reserves. This at heart is fractional reserve banking and was, in fine, a monetary tool that controlled the effective level of debt in the economy by leaving the reserve control with the central banks. The level of debt, and therefore risk in the economy, was ultimately controlled by the central banks. In practice it didn't work that way 1/ banks would emit debt first and then go to the markets to get reserves, which they always got. 2/ banks started unloading the debt in CDOs and recycling the cash thus raised in more debt. In other words, the monetary levels, aka debt, aka level of risk explored was out of control of the central banks. The risk level was too high (say 40x debt to equity). AND IT IS THIS PART THAT WAS PROBLEMATIC.

A super charged Minsky cycle.

The reason is a little thing called the minsky cycle, that says that left to its devices an economy will choose to always increase debt, because it increases prices of assets, which increases return of said assets, which increases return on equity, which increases demand for the debt which .... cycle again. This at first IS A VIRTUOUS CYCLE, resulting in a monetary boom, which, arguably was started under Reagan and "Reaganomics" (which really was a Keynesian program to spend on the military, the national labs etc, with results such as the downfall of communism and the birth of silicon valley as we know it). The problem is that this cycle DOES NOT SLOW DOWN BUT ACCELERATES until the moment where the debt servicing flow is ahead of the real income from the asset. And the problem is that the dynamics are then UNSTABLE IN REVERSE. There is a crash and the cycle restarts. This moment is known as 'fisher moment' and the cycle the 'minsky cycle'.

Abuses within the Minsky cycle, the naked CDS debacle

Whether the Minsky cycle is a positive or a negative is a larger debate (I would say positive actually, modulo the crashes). What was really objectionable in 2008 was some of the more exotic speculation around synthetic CDS and the like that multiplied the bad-debt when it started appearing in the system.

Dodd Frank addresses some of it.

The reason I go through all this background is that in fact the current legislation in fact starts to deal with these off balance sheet instruments. Notice that any legislation that is 'balance sheet' driven (which is the classical way to legislate by numbers) will miss "off balance sheet' instruments, almost by definition. To a large extent they were designed for this 'regulatory arbitrage'. The current legislation starts remeasuring the monetary flows by creating open and standardized markets for these "off the counter" (i.e. opaque) instruments. IT HAS NOTHING TO DO WITH GLASS STEAGALL. We may want to call it that for marketing purposes, however. The new legislation does not ban any product.

Most derivatives serve real world needs.

This last bit I will leave for another day, because it takes a lot of background and education before one can really go about judging these products, but let us just say that most derivatives serve real life purposes and that, by and large, they are beneficial to the economy. It is true however that naked CDS were abused for border line criminal activity. It is also true that Frank Dodd doesn't really try and legislate those and it is certainly true that it shouldn't try and legislate the broader derivatives. Those that call for a blank carpet over it usually have no idea what they are dealing with...

Comments